Gambling Ads Are Now Inside Your Payment Apps

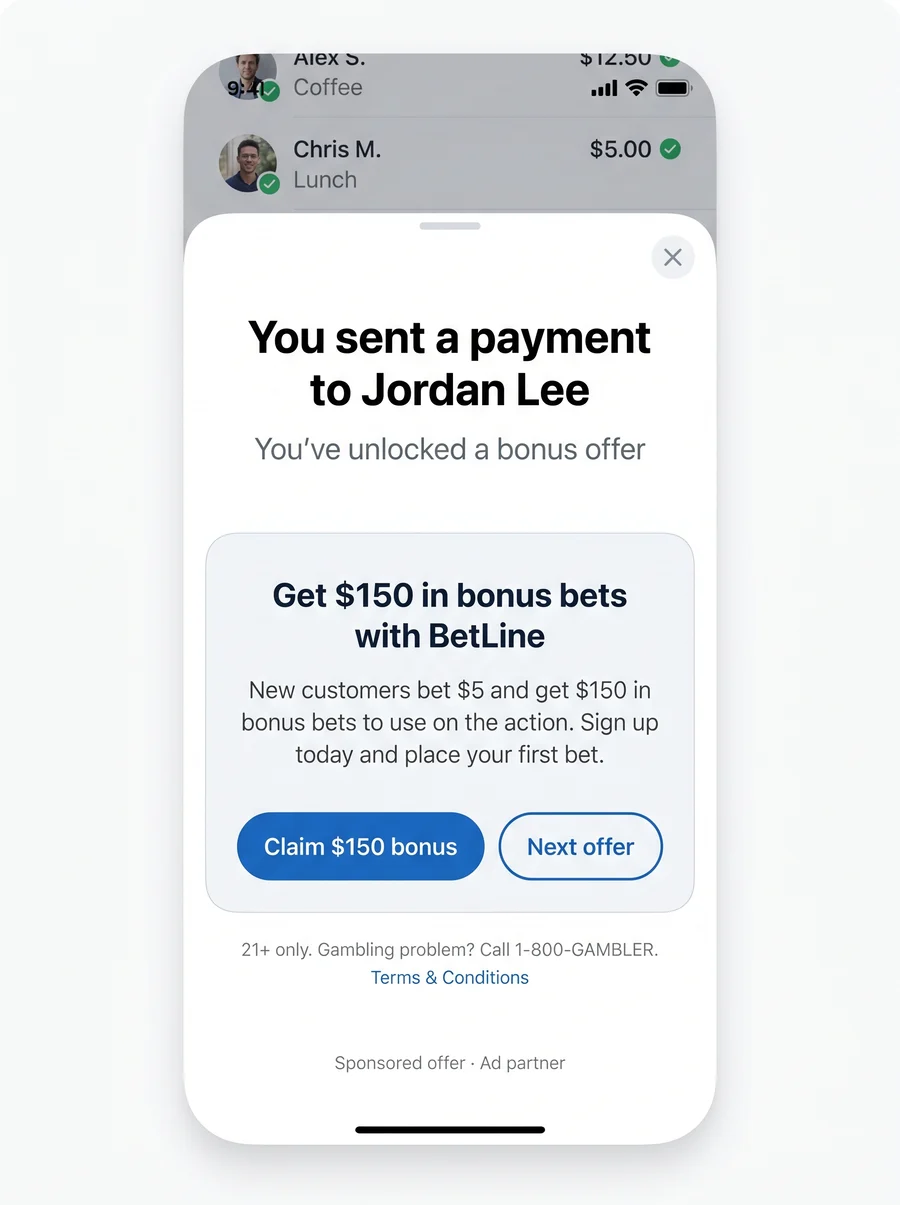

You sent money. The app offered you a bet.

You open a payment app to do something ordinary. Split a dinner check. Pay rent to a roommate. Send a few dollars to a friend. The transfer goes through. And then, before you can close the app, a full-screen card slides up: a sportsbook offer, a large bonus figure, and a single button to claim it. One tap.

I know the moment because I lived it. After sending money on a payment app, my screen filled with a sportsbook offer: a large bonus figure, a one-tap "claim" button, the line "Powered by Rokt," and a small disclaimer at the bottom: "21+ only. Gambling problem? Call 1-800-GAMBLER." I am in recovery from gambling. The app I use to manage my money had just handed me a one-tap path back to the thing I am working to stay away from.

Illustrative reconstruction. The recipient name, the sportsbook, and the dollar amounts shown here are fictional. The pattern is real: a one-tap betting offer surfaced in the seconds after you send money, with a helpline number in the fine print.

This article is not about one operator, one app, or one offer. The specific names are interchangeable. The story is the design pattern: gambling is being injected into everyday financial moments, frictionless and one-tap, inside the apps people open to manage their money. That pattern reaches everyone who uses these apps, including the people in gambling recovery who are most harmed by it.

How a bet ends up on your payment screen

The offer you see is not placed by your friend, and it is usually not placed directly by the sportsbook either. It is sold by an ad network that specializes in what the industry calls the "transaction moment."

The clearest current example is Rokt. In October 2025, eMarketer reported that PayPal partnered with Rokt to serve personalized post-transaction ads to PayPal, Venmo, and Honey users in the US. According to a Sacra industry analysis, Rokt operates an ad network of roughly 3,000 commerce partners and shows third-party offers to people "primed to buy" in the seconds right after they complete an action. Rokt's business model, per that same analysis, is to take roughly fifty cents of every advertising dollar spent across its network. The partners named in coverage of Rokt's network span retail, travel, food delivery, and ride-hailing. The post-transaction screen is valuable precisely because attention and intent are high at the instant a payment clears.

Payment companies are building this into their core product on purpose. PayPal's own advertiser materials describe "Onsite Ads" placed within the PayPal and Venmo apps "during high-intent moments like checkout and P2P transfers," and note that a large majority of surveyed users say they are open to buying things while inside the app. PayPal has been expanding its advertising business aggressively, including a deterministic ad identifier built on what the company describes as 25 billion transactions across more than 400 million accounts, per company materials reported by industry trade press. The financial moment is no longer just a transaction. It is ad inventory.

None of this is hidden, exactly. It is disclosed in fine print and policy pages. But disclosure is not protection. The person sending rent money did not go looking for a sportsbook. The sportsbook came looking for them, at the moment their money was already in motion.

Why this placement is uniquely dangerous in recovery

For most people, a betting prompt after a payment is an annoyance. For someone with gambling disorder, it is a cue delivered at close range, and the science on why that matters is not ambiguous.

Online gambling is more harmful than offline gambling in large part because of its structure. A systematic review in the Journal of Gambling Studies and related research attribute the elevated addictive potential of online gambling to situational and structural features: availability, accessibility, immediacy of reinforcement, and the speed and frequency of play. The World Health Organization, in its December 2024 gambling fact sheet, puts it plainly: because gambling is available online, "it is accessible almost anywhere, at any time, even in places where gambling is prohibited."

A one-tap offer inside a banking app is the purest expression of that structure. It collapses the distance between an impulse and a bet to a single screen tap, with the money already at hand. Recovery, in practical terms, runs on friction: the deleted app, the blocked site, the trusted person holding the passcode, the minutes it takes for an urge to crest and recede. The transaction-moment ad is engineered to erase exactly that friction. It is the opposite of the protective barriers people in recovery work to build.

Impulsivity makes the placement worse. Across the research literature, high impulsivity is one of the most consistently documented risk factors for problematic online gambling. The transaction moment is built to exploit impulse: a large number, a short deadline framing ("new customers"), and a button. For a brain that has spent years learning to act fast on a betting cue, that is not a neutral offer. It reactivates a conditioned response, the same cue-reactivity mechanism that makes gambling ads in live sports spike cravings, except now it is sitting inside the tool you use to pay your bills.

There is a particular cruelty to the location. Financial control is one of the first things gambling disorder takes and one of the last things recovery restores. People in recovery often route their money deliberately, handing financial access to a partner or a counselor, precisely so the money is harder to reach in a weak moment. We wrote a whole guide on rebuilding finances after gambling because that work is slow and hard. To then meet a betting offer inside the banking app is to be ambushed in the one place a person was trying to make safe.

The scale of who this reaches

The reach here is not niche. The National Council on Problem Gambling estimates that 2.5 million U.S. adults (about 1%) meet the criteria for a severe gambling problem in a given year, and another 5 to 8 million (2 to 3%) have mild or moderate problems. NCPG estimates the annual national social cost of problem gambling at $14 billion, including criminal-justice and health-care costs, job loss, and bankruptcy.

Payment apps do not screen for that population, and by design they cannot. The whole premise of the transaction-moment ad is reach: everyone who completes a payment is eligible to see the offer. That means millions of people actively trying not to gamble are being served frictionless betting offers inside an app they cannot easily abandon, because it is how they pay people. A self-excluded gambler can delete every sportsbook app and still meet a sportsbook in their banking app.

This is the same machinery that already saturates other surfaces. The National Consumers League, after collecting more than 100 push notifications over four weeks from the three largest sportsbook apps, found in a July 2025 report that 93% of those notifications contained advertising material, 62% pushed users to place bets, and 50% promoted bonuses or odds boosts. The payment-app placement extends that pressure into a new and more intimate space: not the betting app a person chose to keep, but the financial app they cannot easily live without.

The oversight gap

Here is the uncomfortable part: it is not clear who, if anyone, is regulating gambling ads inside payment apps.

Gambling itself is regulated state by state, and sportsbook advertising is loosely governed by a patchwork of state rules, platform policies, and industry self-regulation. But a payment app is not a sportsbook, and an ad network is not a gambling operator. The placement sits in a seam between regulators. The Federal Trade Commission does not have direct authority over gambling, but it does have broad authority under the FTC Act to police "unfair or deceptive acts or practices." The National Consumers League has argued that aggressive sportsbook advertising aimed at a population likely to include people with gambling disorder "may be an unfair practice prohibited by the FTC Act," and has urged the FTC to take a serious look at it. That argument applies with extra force to a one-tap betting offer delivered inside a financial app, but as of this writing no rule specifically governs the placement.

Meanwhile the surface area keeps expanding. Sports-style betting is migrating into federally regulated prediction markets and brokerage apps that sit alongside where people manage savings, a shift we cover in the rise of prediction-market betting. The common thread is that gambling is being woven into the financial tools of everyday life, in places with fewer gambling-specific consumer protections than a licensed sportsbook would face.

The disclaimer at the bottom of the offer I saw, "Gambling problem? Call 1-800-GAMBLER," is real and the number works. But a helpline number printed under a one-tap "claim" button is not a safeguard. It is an acknowledgment, in fine print, that the product being advertised harms some of the people it is being shown to.

What protects you, and what should change

You cannot fix the ad network. You can reduce its grip on you.

Treat the payment app as a gambling surface, because it now is one. If you are in recovery, the payment app belongs in your protective plan alongside sportsbook and casino apps. Do not assume it is neutral ground.

Turn off what you can. Some payment apps let you limit promotional content, opt out of personalized ads, or tighten ad and privacy settings. These controls are imperfect and easy to miss, but reducing personalized offers lowers how often a betting prompt finds you. Check your app's privacy and notification settings today, not the next time an offer appears.

Add friction back deliberately. The placement works by removing friction, so put it back. Keep gambling blockers active at the device and network level so that even if you tap an offer, the destination is blocked. Consider whether a trusted person holds the keys to your accounts. Slowing the path from impulse to bet is the entire game.

Name the moment when it happens. When an offer slides up, it can produce a fast, physical pull before you have a conscious thought. Name it: "that is a cue, not a decision." Cravings crest and fall, usually within minutes, if you do not feed them. Our guide on recognizing a gambling urge walks through catching the wave early. The offer is designed for the version of you that acts in two seconds. Give yourself twenty.

Do not treat a near-miss as a failure. Feeling the pull when an unexpected betting offer appears is not relapse and is not weakness. It is a conditioned response to a cue that was placed in your path on purpose. The reaction is information about the environment, not a verdict on your recovery.

What should change is larger than any one person's settings. Payment companies could exclude gambling from the transaction moment entirely, the way some platforms already restrict it elsewhere. Ad networks could carve betting out of post-purchase inventory. Regulators could decide that a one-tap sportsbook offer inside a banking app, shown to a population known to include millions of people with gambling disorder, is exactly the kind of unfair practice the FTC Act was written to reach. Until then, the protective work falls to the individual, which is not fair, but is where things stand.

If a prompt like this put you on edge, you do not have to sit with it alone. The 24/7 National Problem Gambling Helpline at 1-800-GAMBLER is free, confidential, and staffed every hour of every day. You can also build a personal plan and find meetings, clinicians, and tools at Cope Compass find-help.

Sources

- eMarketer. (2025, October 23). PayPal taps Rokt to monetize post-transaction moments. emarketer.com. Supports the PayPal/Rokt partnership, the Venmo/PayPal/Honey scope, the post-transaction placement, and the announcement date.

- Sacra. Rokt: the $480M/year ad network behind Uber & Lyft. sacra.com/research/rokt-480m-year-ad-network/. Supports how the transaction-moment ad network works, the ~3,000 commerce partners, the "primed to buy" framing, and the ~50% revenue cut.

- PayPal. Onsite, Offsite & Offer Advertising. paypal.com/us/advertiser/solutions. Supports "Onsite Ads" placed during checkout and P2P transfers and the "high-intent moments" framing inside PayPal and Venmo.

- National Consumers League. (2025, July 28). Advertising sports betting with smartphone notifications: what NCL learned and how regulators can act. nclnet.org. Supports the 93% / 62% / 50% notification figures, the FanDuel/DraftKings/BetMGM methodology, and the FTC "unfair practice" argument.

- National Council on Problem Gambling. FAQs: What is Problem Gambling? ncpgambling.org/help-treatment/faqs-what-is-problem-gambling/. Supports the 2.5 million severe (1%), 5 to 8 million mild/moderate (2 to 3%), and $14 billion annual social cost figures.

- World Health Organization. (2024, December 2). Gambling (fact sheet). who.int/news-room/fact-sheets/detail/gambling. Supports "accessible almost anywhere, at any time," the 1.2% global disorder prevalence, and that around 1 in 8 men experience gambling harm.

- Online Gambling: A Systematic Review of Risk and Protective Factors in the Adult Population. Journal of Gambling Studies. link.springer.com/article/10.1007/s10899-023-10258-3. Supports availability, accessibility, immediacy, and impulsivity as drivers of online gambling harm.

- American Psychiatric Association. (2013). Diagnostic and Statistical Manual of Mental Disorders, Fifth Edition (DSM-5). Gambling Disorder, code 312.31. ICD-10 code F63.0.

- National Council on Problem Gambling. National Problem Gambling Helpline, 1-800-GAMBLER. ncpgambling.org.

Related articles

Find help near you

Cope Compass is free.

Real-time support that learns your patterns and adapts to your recovery over time. The more you use it, the better it understands your triggers.

Try it now